Stand on the ridge of Kimihurura at dusk and you will see cranes silhouetted against a copper sky. Towers rise in Kiyovu. Gated communities push outward past Kinyinya and Masaka. Kigali, once a modest hillside capital, is building itself into one of Africa's most remarkable urban stories — a city where cleanliness, safety, and ambition converge in a rare and powerful combination. Yet for most of the 1.7 million people who call it home, that story is being told in a language they cannot quite afford.

Rwanda's real estate market is booming. And it is, for a majority of Rwandans, almost entirely out of reach.

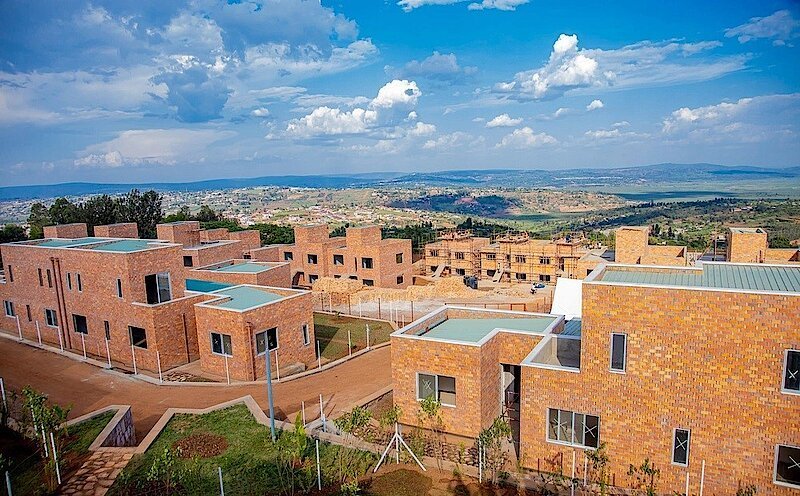

What is property actually worth in Kigali?

Rwanda's real estate sector now contributes an estimated 16 per cent of national GDP. In 2026, a furnished luxury villa in Nyarutarama or Kimihurura commands anywhere from $250,000 to well over $500,000. A two-bedroom furnished apartment in mid-tier suburbs rents for $800 to $1,500 per month. Premium three-bedroom apartments and villas are listed at $2,500 to $5,000 monthly. These are numbers that would not embarrass a mid-tier European city.

A basic cadastral house in areas like Gatsata or Kimisagara begins at RWF 60–70 million (approximately $45,000–$55,000). A mid-market house in a structured suburb sits between RWF 80 and 180 million. Development land near the Special Economic Zone in Ndera trades at industrial-grade premiums.

Are these prices realistic?

For the small class of Rwandans and foreign investors who occupy the top three percent of earners, Kigali's prices are defensible and arguably still undervalued relative to the city's trajectory. Rwanda's economy grew at 9.4 percent in 2025. Political stability, a digitised land registry, a transparent legal framework, and 99-year renewable leaseholds available to foreigners make Rwanda among Africa's most investable real estate markets.

For everyone else — the teachers, nurses, civil servants, small traders, and informal sector workers who constitute the overwhelming majority — these prices are not just challenging. They are structurally exclusionary.

A housing market is generally considered affordable when median home prices do not exceed three to four times median annual household income. In Kigali, the ratio is dramatically worse. A basic RWF 70 million home represents more than 17 years of an average salary — before taxes, food, transport, or school fees. Only about three percent of Rwandan households earn above RWF 1 million monthly.

Six structural forces driving prices skyward

Land scarcity. Rwanda is the second most densely populated country in Africa. Kigali's hilly topography constrains development. Speculative land-banking — holding plots idle in anticipation of appreciation — removes further supply from the market at a time when demand is surging.

The cost of materials. A 35 percent import duty on construction inputs sourced outside the East African Community, compounded by an 18 percent VAT, produces a markup of roughly 58 percent over base costs. Every tonne of cement, every beam of steel arrives at Kigali building sites already made expensive before a wall is raised.

Mortgage exclusion. Commercial banks charge 11 to 16 percent annual interest on home loans and require 20 to 30 percent down payments. Fewer than five percent of Rwandans use bank credit to buy a home. A middle-income household can typically qualify for only a RWF 4 to 10 million loan — far short of the RWF 20–40 million cost of a single bedroom in a formal development.

Urbanisation pressure. Kigali's population grows at over four percent annually. By 2032, the city requires 15,000 to 32,000 new homes each year to absorb in-migration alone. Meanwhile, the Rwandan diaspora — professionals in Europe, North America, and the Gulf — invests actively using dollar- and euro-denominated savings, competing directly with local buyers and bidding prices further out of local reach.

Regulatory costs. Planning permits, environmental assessments, and approval delays collectively add approximately nine percent to a project's total cost before construction begins. These costs are passed directly to the buyer in the sale price.

A supply crisis. The formal affordable segment delivers around 600 units per year against a stated annual need of 18,000 in Kigali alone. A 2018 Rwanda Housing Authority study found the city would need 700,000 new homes by 2028, with 70 percent needing to be affordable. That gap has not closed.

The middle-class trap

Rwanda's housing pain is sharpest in the middle. Teachers, nurses, police officers, and civil servants — those earning RWF 200,000 to RWF 700,000 monthly — earn too much for government subsidies and too little for commercial mortgages. Most rental agreements require three months' advance payment, sometimes a full year upfront. For a family renting at RWF 300,000, that means RWF 3.6 million before move-in day: roughly a full year's disposable income, if any exists at all.

What the government is doing — and what more is needed

The Government of Rwanda is not passive. The Rwanda Housing Finance Project — a $150 million World Bank facility administered by the Development Bank of Rwanda — aims to expand mortgage access for households earning RWF 200,000 to RWF 700,000. Funds are on-lent at a ceiling of 11 percent over 20 years. The Rwanda Mortgage Refinance Company is being established to improve market liquidity.

Flagship projects — Bumbogo, Bwiza Riverside, Busanza, Masaka (Urukumbuzi), Izuba City, and Rugarama Park Estate — are in development. In select schemes, the government subsidises 30 percent of costs for qualifying first-time buyers. New regulations require developments of 20 or more units to allocate at least 20 percent as affordable housing, with a 30-year moratorium on reclassification.

These are creditable efforts. They are not yet sufficient. The World Bank's own implementation reviews note that anticipated housing pipelines have not materialised — primarily because infrastructure delays make affordable development commercially unattractive to private developers.

What must change — a blueprint for action

The government must reduce import duties on construction materials used in certified affordable housing projects. A targeted exemption on cement, steel, and roofing inputs would directly reduce unit costs. Infrastructure provision — roads, water, power — to unlocked land parcels must be accelerated; this is the single most-cited bottleneck in Rwanda's housing pipeline. Mortgage products for households earning below RWF 200,000, structured as rent-to-own or microfinance housing loans, must be developed urgently.

Private developers must invest in alternative construction technologies. Aerated autoclaved concrete, prefabricated modular units, and 3D-printed structures can reduce build costs by 25 to 40 percent against conventional methods. Developers who master these now will own the affordable segment as it scales — and that segment is enormous.

For investors, Rwanda's fundamentals are among the strongest on the continent: GDP growth of 7 to 11 percent, a transparent land registry, 99-year leaseholds for foreigners, and a government with a proven track record. The risk is not political. The risk is building for the wrong market. Investors who chase the luxury segment in a country of $334 average monthly salaries are building for a thin pool that is already well served. The underserved market — the RWF 200,000 to RWF 700,000 monthly income cohort — is where volume and long-term returns lie.

A city is not its skyline. It is its teachers and nurses, its market traders and civil servants, its young graduates. If Rwanda builds a Kigali that these people cannot afford to live in, it will have built a beautiful city for someone else. The land of a thousand hills can surely build a home for all who climb them.